Buying a used car on finance is a practical choice for many Indian buyers who want the experience of personal mobility without the full price tag of a new vehicle. The used-car loan market has grown significantly, with lenders offering competitive products that make pre-owned car ownership accessible across income levels. However, the financing process for used cars comes with a few nuances that, if not understood in advance, can result in a higher-than-expected total cost or unexpected charges during documentation.

Here you will learn how to accurately calculate the EMI on a second-hand car loan and which charges to watch for during the application process.

How to Calculate Your Used Car Loan EMI Correctly

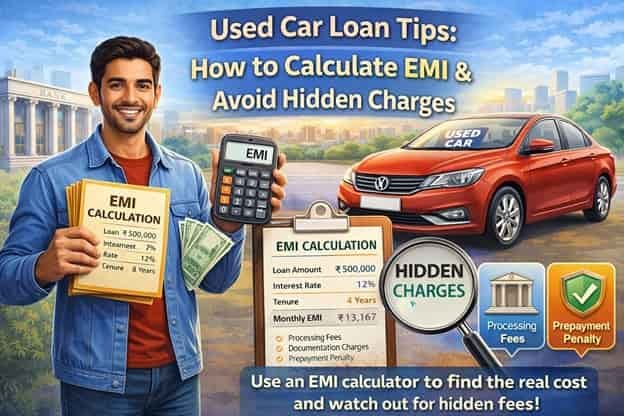

The EMI on any loan is determined by three variables: the principal loan amount, the interest rate, and the tenure. For a used car loan, the principal is not simply the purchase price. It is the loan amount the lender agrees to disburse, based on their independent valuation of the car and the applicable loan, typically ranging from 1 to 50 lakh.

The starting point for any EMI calculation is therefore the lender’s valuation of the specific car, not the seller’s asking price. If the seller is asking ₹5 lakh and the lender values the car at ₹4.5 lakh at an 80 percent LTV, the maximum loan is ₹3.6 lakh. Using a used-car loan EMI calculator with the correct loan amount, expected interest rate, and a realistic tenure will give you an accurate estimate of the monthly outflow.

Choosing the Right Tenure

Used car loan tenures are typically capped at up to 6 years for relatively newer cars and may be shorter for older vehicles. The lender caps the tenure based on the car’s age at the time of the loan.

Before fixing the tenure, use the EMI calculator to compare monthly outflows across different tenures. If a shorter tenure is manageable, it can help you save significantly on total interest over the life of the loan. Choosing the longest available tenure simply to minimize the monthly EMI increases the total interest paid without any corresponding benefit.

Hidden Charge 1: Processing Fee

Every used car loan comes with a processing fee charged by the lender to cover credit assessment, document verification, and vehicle valuation. This fee is non-refundable and typically ranges from up to 2.95% of the loan amount + GST.

For a ₹3.5 lakh loan, a 2 percent processing fee of ₹7,000 is paid upfront before the first EMI. This effectively increases the overall cost of the loan. Always ask for the exact processing fee in writing before signing the loan agreement.

Hidden Charge 2: Vehicle Inspection and Valuation Fee

Lenders typically conduct an independent valuation of the used car before approving the loan. The cost of this inspection is usually charged to the borrower and can range from ₹1,000 to ₹3,000, depending on the lender and location.

This charge is separate from the processing fee and is sometimes not mentioned clearly in the initial loan discussion. Asking specifically about the valuation fee before proceeding can help you avoid surprises at the disbursement stage.

Hidden Charge 3: Insurance Bundling

Some lenders offer or require a loan protection insurance policy bundled with the second-hand car loan. The premium is typically added to the loan amount, increasing both the principal and the total interest paid over the tenure.

Borrowers should clarify whether the insurance is mandatory or optional. If it is optional, they should separately evaluate whether coverage is needed and compare the cost of a standalone term plan, which is generally more cost-effective for similar level of protection.

Hidden Charge 4: Prepayment and Foreclosure Fees

If there is any chance the loan will be repaid early, the prepayment policy deserves attention before signing. Most lenders apply a prepayment charge of 6% of the prepayment amount within 12 months of the first disbursement date. Whereas, 5% of the part-prepayment amount after 12 months from the date of the first disbursement, or 6% of the outstanding principal if the loan is foreclosed before the contracted end date.

Borrowers who expect to foreclose the loan early should factor this charge into the total cost calculation or negotiate for a loan with more flexible prepayment terms before committing.

Conclusion

A second-hand car loan can be an excellent financial tool when taken out with full awareness of the total cost structure. Calculating the EMI on the correct loan amount, choosing a tenure that balances affordability and total interest, and asking specifically about processing fees, valuation charges, insurance bundling, and prepayment terms before signing are the steps that helps the borrower to make a well – informed decision.

Taking just 30 minutes to do this groundwork before visiting the lender or dealership is always time well spent.

Santosh Kumar is a Professional SEO and Blogger, With the help of this blog he is trying to share top 10 lists, facts, entertainment news from India and all around the world.